Field Notes (e.13): Reality checking real estate (Home size edition)

A macro analysis of Sacramento home price per square foot performance.

Hi All,

I hope this finds you well. Before diving into this edition of the newsletter I wanted to let you know that I’ve started using Twitter to share real-time thoughts, charts, and analysis about economics, real estate, emerging tech, and #Bitcoin. This newsletter will still be the home for my longer-form writing but if you’re on Twitter and love charts, come say hi 👋 @wrightology.

Without further ado, let’s talk a bit more about real estate!

In Reality checking real estate, I analyzed residential real estate performance using average home price data. As I noted in the original piece, the analysis didn't account for one critical variable — home sizes:

The rate of increase of the current cycle slowed noticeably starting in 2014. One possible reason is home builders began supplying more smaller homes, which helped dampen price growth and improve affordability (source, source). Median home price per square foot would be an interesting topic for future analysis.

This follow-up edition revisits the previous analysis with the goal of incorporating median home size data to answer a simple, tongue-in-cheek question: Does size matter?

The more variables you can account for the more precise an analysis will be. I was confident that the original average price data analysis produced directionally correct conclusions about the market cycles. But, I wanted to know if the current cycle’s wider, more rounded top was valid (as it’s distinctly different than past cycle tops), or if it was a side effect of unaccounted changes in home sizes.

Let’s dive in!

A quick note about the source data

First, I want to give a shout-out and thank you to Ryan Lundquist for providing the Sacramento Area median home size source data for this analysis. He’s an appraiser, data analyst, and writes an exceptional blog about the Sacramento real estate market (link to his blog). He’s also a great follow on Twitter (@sacappraiser).

Second, the national median home size data is sourced from the US Census Bureau which publishes an array of historical construction and real estate data.

Lastly, local home size data isn’t generally available, so this analysis focuses specifically on the Sacramento market. As I always stress, real estate is highly localized, so mileage may vary if one attempts to apply these conclusions to another market.

Home size trends

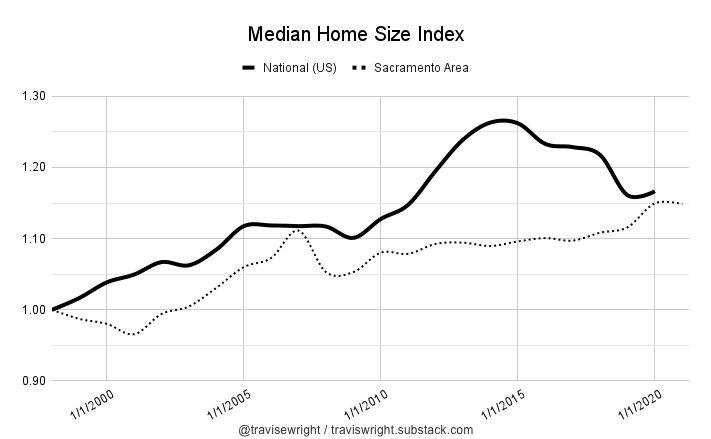

To begin, here’s how median home size has changed since 1981 (Sacramento data starts in 1998):

To make it easier to compare, here’s the same data indexed to 1998:

Observations

At present, home sizes have increased by ~15% since 1998.

Nationally, home sizes ballooned ~16% between 2009 and 2014.

Home sizes have fallen meaningfully since 2014 (which aligns with the sources I linked to in the quote above from the original analysis)

With the exception of the near parity in 2007 and 2020 (both mid-correction years), Sacramento Area home size increases have lagged behind the national trend.

Performance Analysis: Price Per Square Foot

Next, let's incorporate the Home Size Index data into the original Performance Index model. M2 Money Supply is included for reference (red):

Observations

As is the case with the average price data, local markets tend to demonstrate more amplified cycles than the national trend in price per square foot terms.

M2 Adjusted Median Home Price Per Square Foot

Now let’s look at the Performance Index in terms of purchasing power. Adjusting the median home price per square foot performance data for M2 Money Supply growth produces the following:

Observations

As is the case with the average price data, homes values have meaningfully underperformed M2 growth in price per square foot terms.

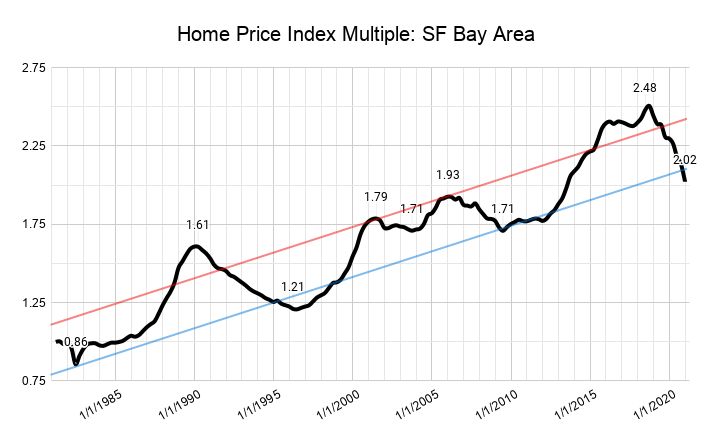

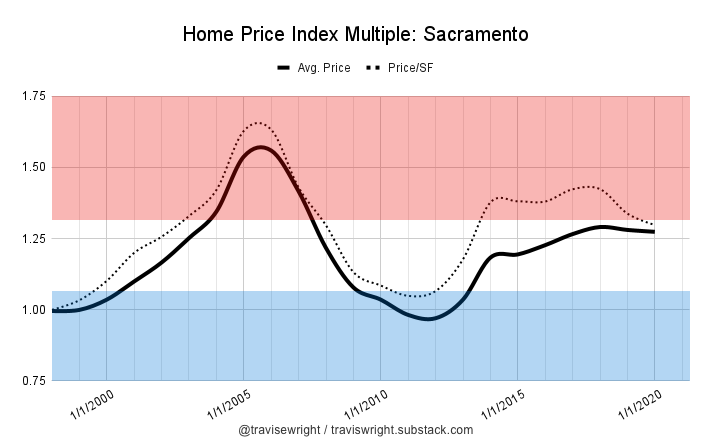

Home Price Index Multiple: Price Per Square Foot

Finally, let’s take a look at my favorite metric for analyzing local market cycles: The Home Price Index Multiple (HPIM).

The HPIM is an investing metric I created that tracks the ratio of a local market’s price index to the national price index (I first introduced the HPIM in the original Reality checking real estate analysis).

The idea is that the national data sets the base trend for the Single-Family Home asset class and local markets will cyclically outperform or underperform the national trend. The HPIM makes local market cycles much easier to identify and also makes it easy to see if a local market is closely matching the national trend (flat channel, like Sacramento), or outpacing the national trend (positive sloping channel, like SF).

{kind=link}

In order to see the differences, I plotted the Average Price and Price Per Square Foot versions of the HPIM together (indexed to 1998):

Observations

You’ll notice that the Price Per Square Foot version is similar in nature to the average price version, but shifted higher. It’s difficult to draw broad conclusions not having the 1991 cycle data to compare against. But, the key difference is that the high of the current cycle successfully reached the overbought (red) zone in Price Per Square Foot terms. Thus, the market could be entering a consolidation period.

Also, this cycle’s more rounded topping pattern (versus the more swift and pointed previous cycle peaks shown in the original analysis) is similar in both the Price Per Square Foot and Average Price versions. The peaks are slightly more amplified in the price per square foot version, which is the type of increased clarity I was hoping to see.

Conclusions

In closing, I’d answer the original question this analysis set out to answer (Does size matter?), as follows:

Yes, accounting for home size matters.

The deviations between Sacramento Area home sizes and the national data set were meaningful for the majority of the post-1998 period. This meant accounting for home size increased the precision and clarity of the local market analysis. This added precision is especially helpful when assessing the current cycle because it isn’t dramatically overbought (yet) by historical standards.

Lastly, my base case interpretation of the above is that nominal home prices are likely to remain elevated, consolidate horizontally, then ultimately push higher (versus experiencing a dramatic correction a la post-2005).

A few additional data points behind my thesis: Months supply inventory is still historically low, purchaser debt levels very healthy, and double-digit annual monetary debasement is likely to continue for the foreseeable future. A macro top in housing would likely coincide with inversions of those signals. Until then, the weight of the evidence points to up.

That said, the current economic order is one of relativity (see Relatively speaking for more on this) and housing will likely continue to meaningfully underperform in purchasing power terms compared to other fixed supply assets like equities or Bitcoin (see the “Looking Forward” section at the end of Reality checking real estate for my expanded perspective on housing.)

Until next time,

Travis / @wrightology

P.S. — If you know someone who would enjoy being in the loop, please feel free to spread the word by sharing this email or this page.

New to the list? Browse past entries here.